Passive Wealth Generation: From Zero to a Million Dollars in Five Measured Steps

Caption: Nest egg--where wealth begins. . . . [Photo credit]

Caption: Nest egg--where wealth begins. . . . [Photo credit]In our capitalist culture everyone wants to grow wealthy--to retire early, to feel more financially secure, or just to join society's upper echelon as measured by net worth. However, if you are like most people, you have a hard time getting started on the road to riches and an even harder time sticking on course.

Over the upcoming month, I will present an easy-to-follow plan that anyone with financial discipline can follow "in their spare time." It is a passive investing strategy, designed to complement your primary source of income from your "real job." Simply put, passive investing--when properly executed--can be highly rewarding. The approach I describe is, in my opinion, the best way to maximize net worth, while concurrently pursuing a satisfying career and favorite hobbies and spending quality time with friends and family.

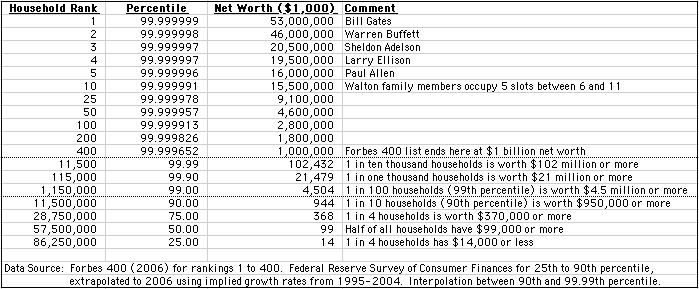

The plan itself is really a "no brainer," so much so that you'll probably feel as if you've previously heard much of what I am going to say. If you are fortunate enough already to have a net worth exceeding a million dollars, this discussion is not intended for you (though if you continue reading, you might run across some of the same thinking that got you to where you are today). On the other hand, if you are a member of the overwhelming majority--the 90% of all American households who are not yet millionaires--I encourage you to read on. (For a summary of the wealth distribution among American households, see this table in an earlier post here.)

From the outset, I emphasize that this is NOT a "get rich quick" scheme. It will not make you into a millionaire overnight. It will not allow you to retire tomorrow. It does not promise spectacular 1000% and higher annual returns. It is not a magic formula for creating "something from nothing," implementing "no money down" methods, leveraging "other people's money" or deluding yourself into similar wishful thinking. Nor does it promise to turn you into the next Bill Gates, Warren Buffett or Sheldon Adelson.

Instead, my recommended plan is a slower-paced, highly practical approach to growing wealthy in the most predictable manner possible. It offers an eminently feasible way to start from zero net worth and become a millionaire within the foreseeable future, within your own lifetime and conceivably even within the next 15 years (by the year 2022). I will explain how to take a measured approach to risk and sidestep the "poor house" in the process.

Here are the basic steps of the plan, just five in total:

- Save at least $1,000 a month

- Set realistic return expectations

- Invest in equities

- Minimize fees, expenses and taxes

- Stay on course

I will cover the first point today and take up one additional point each week for the following four weeks.

Starting with a Savings "Seed"

"You gotta have money to make money," said a college classmate of mine, citing a rich uncle or other such role model. Having marched through school and a successful career over the past few decades, and now hovering post-career and pre-retirement, I have had the opportunity to see and experience first-hand how making money works in real life. Personally, I know many colleagues who have accumulated enough of a "nest egg" in a couple of decades of employment, enough so that they are now able to live off of their savings and investments, and no longer "need" to work (even though many choose to continue working).

Now, there are two sides to saving:

a) Income side: Working to earn money, and

b) Expense side: Exercising fiscal discipline by living within one's means.

Of course, as everyone knows, savings are the result of managing your personal finances so that your income exceeds your expenses.

I recall my later college years in graduate school in the 1980s when I worked as a teaching assistant earning about $5,000 a year (along with a tuition waiver), which allowed me to pay about $200 in monthly rent for a small room in a group house, cover food and miscellaneous expenses (books, an occasional movie, etc.), and still save over a thousand dollars a year. Upon graduation, when I took a job in New York City, my rent rose more than four-fold to $900 a month, but my salary more than compensated for the increase in my cost of living, enabling me to save a sizeable chunk of my earnings. Surely, both as a student and in the early part of my working career, I could have lived in more luxurious accommodations and pursued a more extravagant lifestyle, but I chose not to. Deliberately, I decided to live within my means, adjusting my lifestyle to make sure that I could save at least 10% to 20% of my income.

Just as acquiring wealth begins with fiscal discipline, which is really a mental and emotional balancing act between needs and wants, in many ways "being wealthy" is also a mindset. People who live paycheck-to-paycheck without saving any money are not wealthy, regardless of how much they earn. Conversely, people who are able to put aside a portion of what they earn, however modest their salary may be, either are "wealthy" (in the sense that they are able to buy more than they need, but choose not to spend all that they earn) or at least have a reasonable chance of one day becoming wealthy (as measured more traditionally by net worth).

One's first objective on the road to wealth, then, should be to start saving, which really means educating or training yourself to work a job that generates sufficient income to support your lifestyle and allows you to save a significant portion of each paycheck. Often, it can also boil down to focussing on the expense side by moderating your lifestyle so that at least 10% to 20% of your take-home pay accumulates in your bank account rather than disappearing as discretionary spending (ever consider that maybe you really don't need your jolt of caffiene from Starbucks today?).

Putting savings into a global context, it is interesting to compare the U.S. to other countries in terms of propensity to save. The bar graph below shows results of an ACNielsen survey polling respondents in various countries on how they use their "spare cash." As might be expected, given that the "average American" has a savings rate close to zero, the U.S. has a very low propensity to save. In the results of this survey, the U.S. ranks towards the bottom of the list way down in 33rd place among 38 nations. The countries with the highest propensity to save are all in Asia: India, Taiwan, Singapore, Indonesia, Philippines, Hong Kong, China, Malaysia, Thailand, Japan. Although now is not the time to go into specifics, my guess is that there is a fairly high correlation between savings rate and GDP. Suffice it to say that a regular savings plan is a good starting point for anyone who wishes to boost their "personal cumulative net GDP" (i.e., net worth).

(Click graph to enlarge)

(Click graph to enlarge)For the purposes of our discussion, let's assume that any American seriously interested in building wealth is able to save $1,000 each month, for without this prerequisite savings "seed" it is truly difficult to build significant wealth. So, here I am not referring to someone working an unskilled labor job (e.g., flipping burgers at McDonald's full-time) and earning a minimum wage of $10 per hour, or $1,700 a month (about $20,000 a year), since admittedly living on just $500 a month after taxes (in order to save $1,000 a month) would be quite challenging. Our discussion does, however, encompass this same proverbial fast-food worker who has sufficient motivation and foresight to enter a local community college and begin training himself for an entry-level position paying $20 per hour, or $3,400 a month (about $41,000 a year). At this higher income level, saving $1,000 a month, or about one-third of one's take-home pay, becomes a very realistic proposition, since it is possible for individuals and even small families to live on $2,000 a month in most cities by being frugal consumers, i.e., choosing housing, food and transportation carefully and eliminating unnecessary expenses. For anyone completing a four-year college or obtaining a higher degree, earning more than $20 per hour becomes increasingly likely, making saving more than $1,000 a month not just possible but almost expected. . . .

For the moment, my advice on what to do with your $1,000 a month savings "seed" is literally to put it in the bank. Currently, with the yield curve "inverted" (i.e., short-term interest rates higher than long-term rates), many banks are offering savings accounts with very attractive interest rates of around 5% per annum. These accounts are FDIC-insured, offer full liquidity, have no effective minimum balance, and carry no monthly fees. A few examples I am familiar with are the online savings and free checking packages offered by Citibank and Washington Mutual, and a stand-alone savings account offered by E*TRADE Bank. Other banking alternatives are listed at Bankrate.com. You might also wish to check the ads in the business section of your local newspaper for any attractive offers.

Next week: Setting realistic expectations on investment performance

posted by Lloyd Sakazaki at 5:58 PM

![]()

![]()

{kind=link}

10 Comments:

Check out another beautiful blog site georgiesinvestments.blogspot.com

Great! I love your Blog.

Rgds,

Zoe

Malaysia

Its great to see all the ideas

You may need to see this. FREE e-book.

http://www.income4beginners.com/index.php?uid=7197

I found your blog very informative and written in lucid manner. Hope to read more posts..

I will present an easy-to-follow plan that anyone with financial discipline can follow "in their spare time.

MyInvestorsPlace - trading, value, investing, forex, stock, market,technical, analysis, systems

I absolutely adore reading your blog posts, the variety of writing is smashing.This blog as usual was educational, I have had to bookmark your site and subscribe to your feed in i feed. Your theme looks lovely.Thanks for sharing.

trade4target

It sounds a little strange to me to refer to wealth as passive.

Forex Investment Capital - 200% daily for 30 days

Plan Deposit Amount (US$) Daily Profit for 30 days

Bronze $300-$4,999 50%

Silver $5,000-$19,999 75%

Gold $20,000-$49,999 120%

Platinum $50,000-$500,000 200%

Investing Forex PerfectMoney Investment

http://www.forex-investment.biz

Investing in insurance

http://www.payinghyiponline.com/Forex%20Investment.html

Invest Just $5 (Rs. 325) to Earn $5 million (38 Crores) Easily and quickly with a Global forced Unique Auto-fill Plan Start Making HUGE money Easily and Quickly with our Power Team.

Thank you for sharing such great information. It is informative, can you help me in finding out more detail on online savings plan, i am interested and would like to know more about this field and wanted to understand the basics of online life insurance policy

Post a Comment

<< Home